Start each business day with our analyzes of the most pressing developments affecting markets today, along with a curated selection of our latest and most important news on the global economy.

Global banks face divergent results

Global banks face a range of risks and opportunities from short-term variables arising from deteriorating macroeconomic and credit conditions and long-term considerations including geopolitical shifts and climate change.

A range of risks complicate the outlook for the global economy and the lenders operating in it. The shock of the Russian-Ukrainian war and the sanctions have pushed up inflation, putting additional pressure on major central banks which are reverting to existing monetary policy with a series of interest rate hikes. With global growth looking likely to slump in the near term, the physical risks of climate change – and banks’ exposure to them – could fuel future tensions.

While banks operating in Russia and Ukraine have suffered consecutive months of heavy losses and high provisions for loan losses, other banks in Europe and around the world have had limited direct exposure to its financial consequences because the exposure of foreign banks in monetary terms and as a proportion of total assets according to S&P Global Market Intelligence and S&P Global Ratings. Other banking systems have also been able to withstand geopolitical disruptions. Research by S&P Global Ratings found that in the Gulf Cooperation Council, banks have shown resilience through three decades of political shocks in the region. But elsewhere, the international community’s sanctions on Russia have prompted investors to wonder whether the United States could ever take similar action against Chinese banks, which would pose high-impact risks, according to S&P Global Ratings. And external geopolitical pressures as well as internal political uncertainty continue to strain the Brazilian banking sector.

“Political disruptions tend to trigger investor risk aversion, leading to higher funding costs or possibly capital outflows from banking systems into high-risk markets, even when the events are unrelated to them,” said S&P Global Ratings in a study released today.

Meanwhile, rising interest rates are likely to have diverging effects on different regional banking systems, hurting some while helping others. Australian banks could remain resilient to changing conditions, while Japanese banks could face deteriorating asset quality, widening profitability spreads and heightened credit risk. Latin American banks face difficult operating conditions. According to S&P Global Ratings, tighter monetary policy could benefit banks’ net income in the euro zone, Saudi Arabia, South Africa, the United Kingdom and the United States.

And in the long term, the consideration of climate risks by global banks is likely to expand and be given the same weight as macroeconomic and credit risks.

“In terms of financial stability, the soundness of the financial system may be affected by climate change, when balance sheet assets are concentrated in areas affected by increased damaging weather events (such as storms, floods, fires forest loss and droughts) or chronic physical risk (e.g. sea level rise and changing temperature patterns),” S&P Global Ratings said in a recent economic study. if the transition accelerates, banks’ balance sheets could be affected by ‘stranded assets’, i.e. ‘brown’ assets such as fossil fuels that will no longer be used as the economy transitions to greener production processes could see a sharp decline in value.More generally, climate-related shocks are also likely to affect the dynamics of growth and inflation, and therefore the conduct of monetary policy.

Today is Wednesday, June 22, 2022and here is today’s essential intelligence.

Written by Molly Mintz.

Economy

Economic Research: Emerging Markets: Where’s the Sector Slack?

Emerging markets are facing a tough time as they weather tighter monetary policy in the US, the fallout from the Russia-Ukraine conflict and the impact of COVID-19 related lockdowns in China. These dynamics threaten to set back economic recovery from the downturn of the pandemic, which in most emerging countries is far from over as these new challenges emerge.

—Read the report of S&P Global Ratings

Access more information on the global economy >

Capital markets

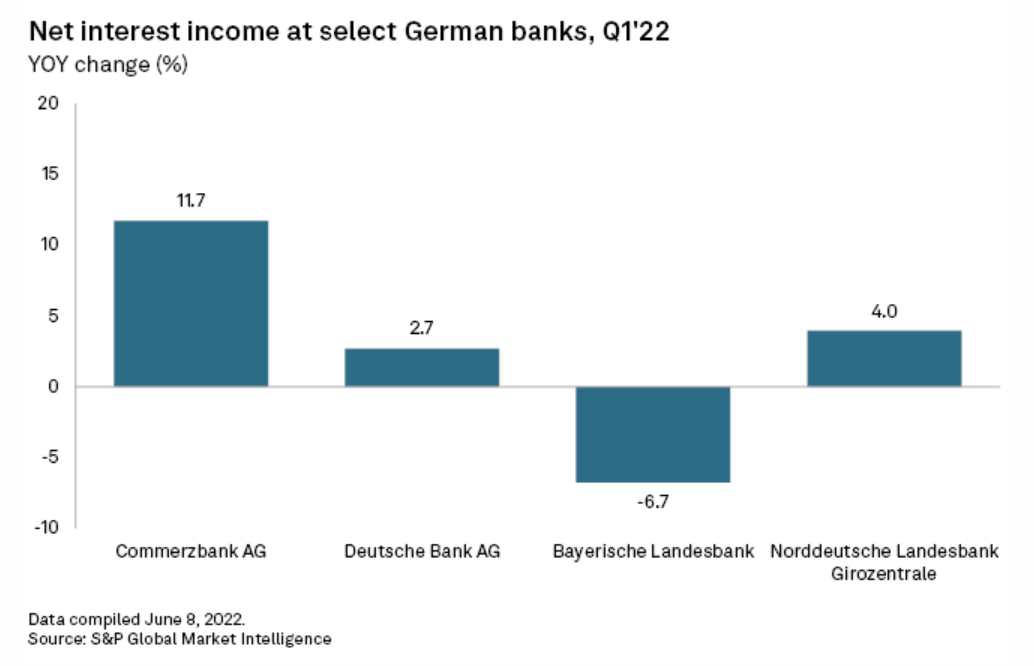

Germany’s big banks expect higher profits in 2022 thanks to ECB interest rate hike

Some of Germany’s biggest banks expect interest rate hikes planned by the ECB this year to boost revenues and mitigate the negative effects of the war in Ukraine and the global economic slowdown. The ECB said it would end its long-standing negative rate policy in July and should gradually raise its key deposit rate to zero by the end of 2022. The deposit rate moved into negative territory in June 2014 and has been at -0.5% since September 2019.

—Read the article by S&P Global Market Intelligence

Access more information on capital markets >

International trade

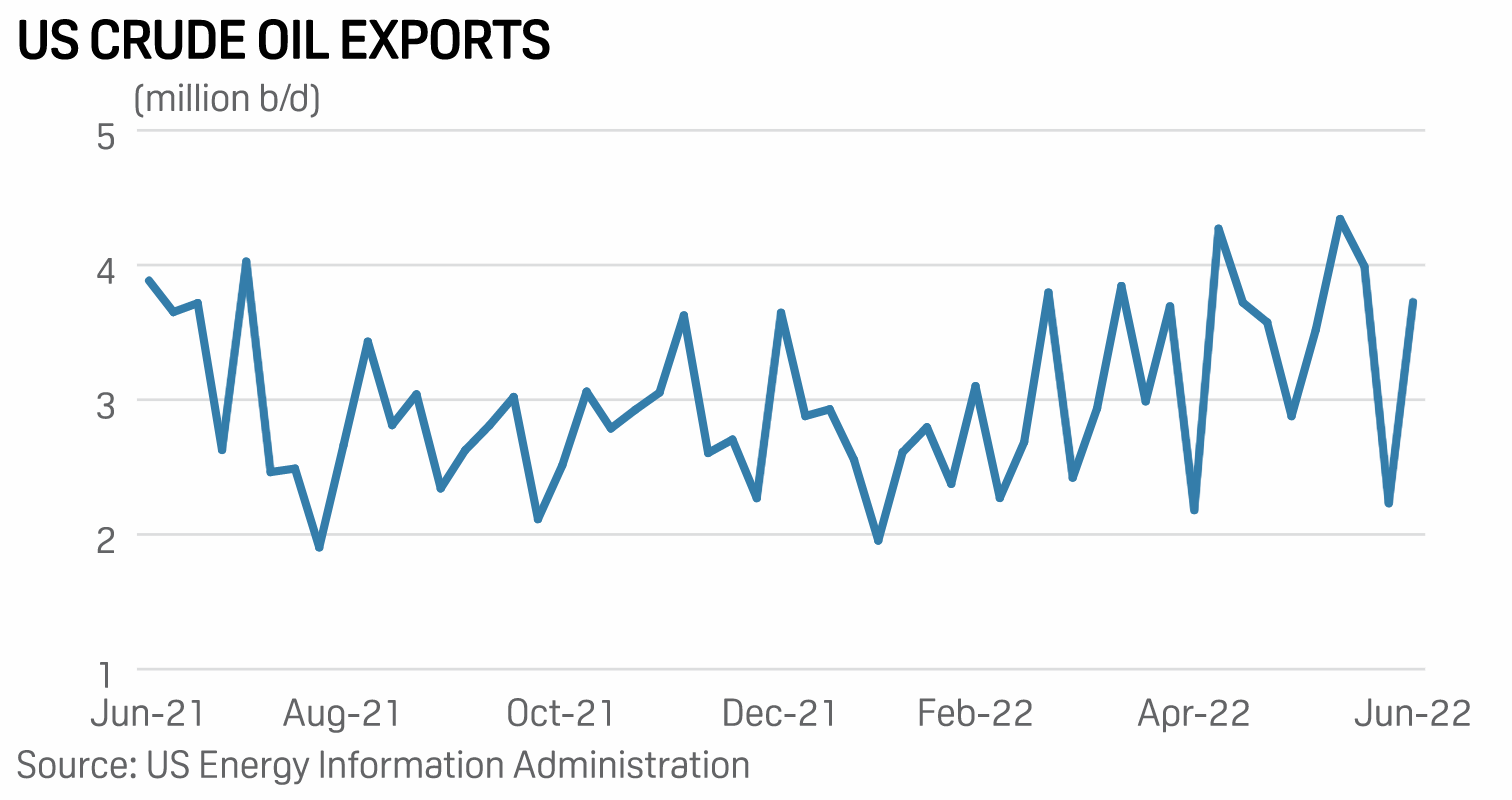

Food for thought: market must take into account all the costs of the disruption of oil flows in Russia

The Western boycott of Russian barrels will be the ultimate test of the oil market. While it has an impressive track record of adapting to unthinkable shifts in business models, from self-imposed embargoes on US exports to sanctions on Iranian and Venezuelan crude, the stakes and costs have never been higher. . The marketplace is already doing what it does best to bring together new buyers and sellers and strengthen existing relationships, but on a scale rarely seen before.

—Read the article by S&P Global Commodities Outlook

Access more information on global trade >

ESG

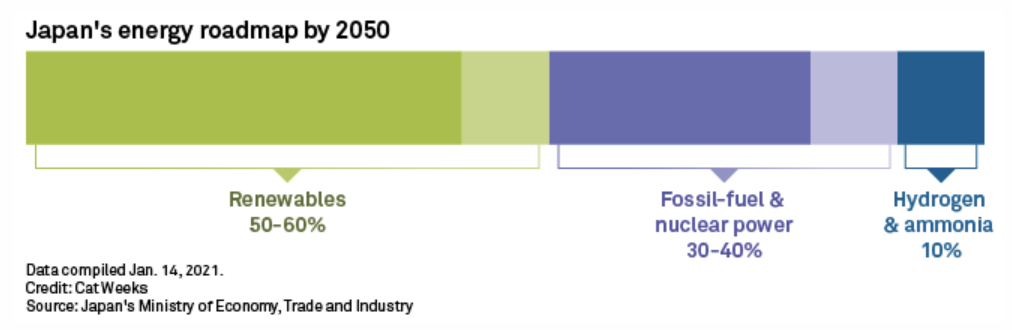

Japan’s $148 billion transition green bond plan will be a tough sell to investors

Japan will likely offer higher yields and greater disclosure of the use of funds to attract investors to its planned “green transition” sovereign bonds as it accelerates carbon neutrality efforts. Investors will need higher yields to compensate for the low secondary liquidity of transition bonds due to low issuance. Global transition green bond issuance totaled $4.4 billion in 2021, up 33% year-on-year, although it represented less than 1% of the $522.7 billion green bonds issued the same year, according to Climate Bonds Initiative.

—Read the article by S&P Global Market Intelligence

Access more information on ESG >

Energy and raw materials

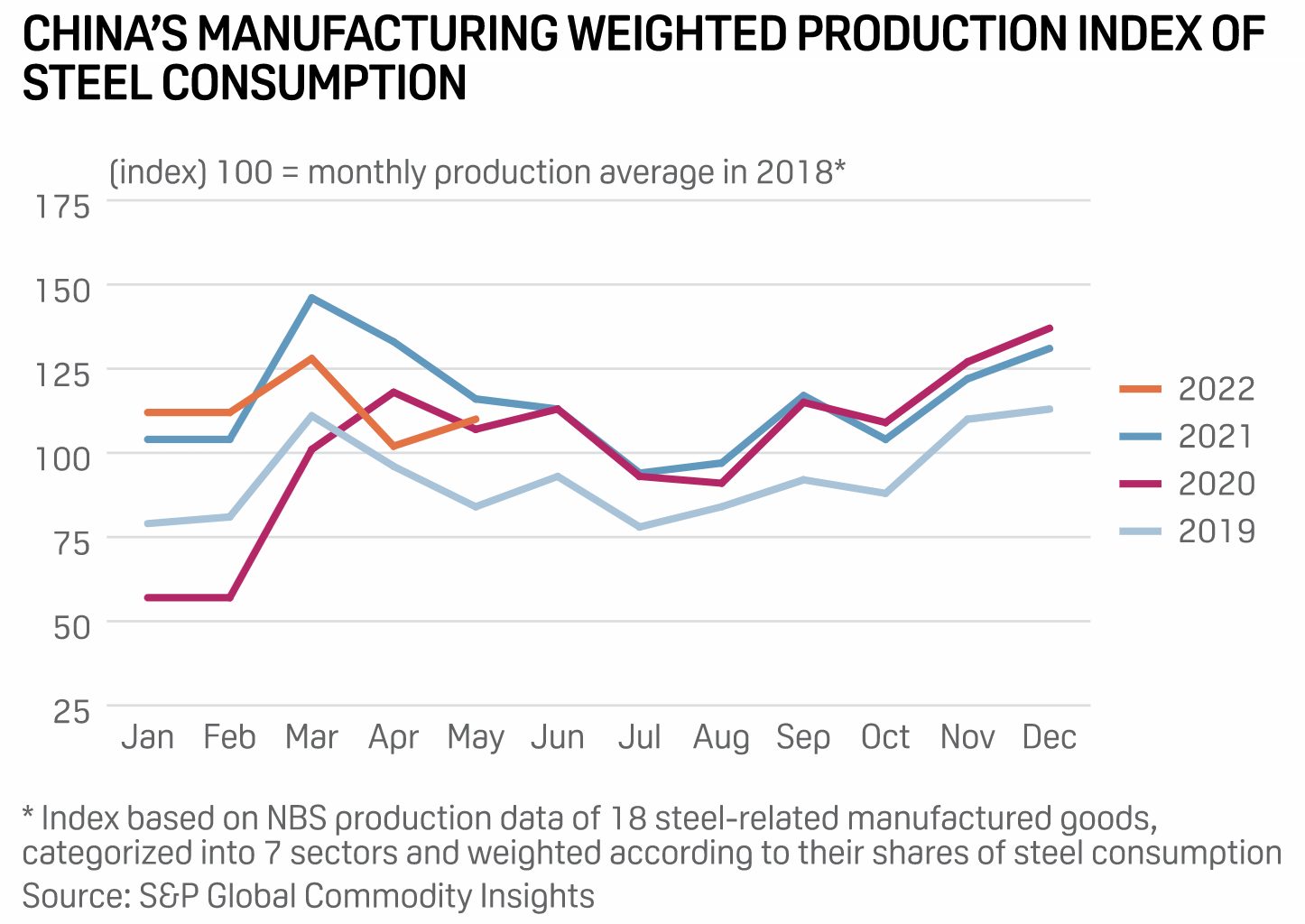

China’s manufacturing recovery pace remains weak, hurting steel demand

China’s manufacturing index for steel consumption produced by S&P Global Commodity Insights stood at 110 points in May, up 9 points from April, but still down 5 points from the same period of 2021. Despite further improvement seen in China’s manufacturing activity in June as it contained a pandemic resurgence, the strength of the recovery has remained slow, leading to the recent sharp drop in prices of steel, industry sources said.

—Read the article by S&P Global Commodities Outlook

Access more information on energy and raw materials >

Technology and media

Listen: Next In Tech | Episode 70: Robots on the Move

While the company has moved away from Robby the Robot being its image of robots, there’s a more helpful nuance. Senior Research Analyst Ian Hughes returns to discuss a Nine Levels of Autonomy Model with host Eric Hanselman and the effects on robotic technology applications. Autonomous vehicles are just the beginning, and many enabling technologies are in their infancy, but digital twins play a key role in shaping the patterns that drive robots and connect them to digital domains and metaverses.

—Listen and subscribe S&P Global Market Intelligence

Access more information on technology and media >

Comments are closed.