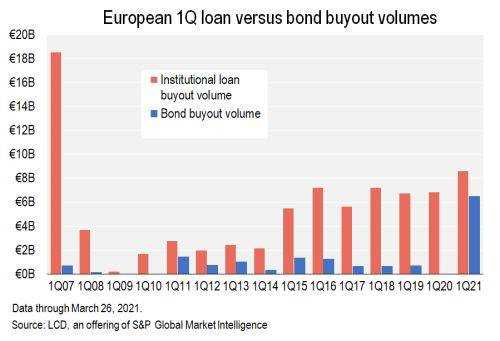

The first quarter of 2021 was the busiest opening of the year for debt buyout lending volume in Europe since the global financial crisis, and also hosted the largest first quarter LBO bond supply ever. recorded. “The first quarter provided the most constructive image we’ve seen for financings since the start of the pandemic,” said a senior banker.

The surge in buyout emissions in the first three months of 2021 illustrates how markets have recovered during the year since the COVID-19 crisis – and the market closures that followed – hit hard. . “At the end of March last year, we were worried about a liquidity crisis, but thanks to state support and the intervention of sponsors, the tightening never came,” says a financing specialist in a private equity firm. “We are now in better shape than I could have ever imagined, and with the strongest emission window that I have seen in a very long time.”

Comparing the first quarter of 2021 to the first quarter of 2020, it is clear that while the funding markets have now returned to strength, there are key differences in buyout funding before and since the outbreak of the pandemic. . To be sure, there is now a closer scrutiny of assets regarding COVID-19 exposure, while issuers in sectors such as hospitality and travel have been particularly affected – although sources point out that if borrowers can prove their resilience and illustrate a roadmap to recovery, then the support is available.

Bonds at stake

Another important change is that bonds played a much larger role in financing buyouts in the first quarter of 2021 than during the same period in 2020. For example, Advanz Pharma Corp Ltd. Jersey turned to the bond market for the bulk of the funding. The acquisition of Nordic Capital, with a 305 million euro term loan and a two-tranche bond transaction equivalent to $ 1.02 billion, while the largest bond buyback of the quarter came from the chain of UK supermarkets ASDA Group Ltd., which backed its £ 6.6 billion takeover. the company by Issa Brothers and TDR Capital with a term loan of 845 million euros, 2.25 billion pounds of covered bonds and 500 million pounds of unsecured bonds. Asda’s secured notes were the largest single-tranche issue ever in the European high-yield market and the largest single-tranche sterling offering.

|

Indeed, European private equity sponsors note that high yield issues are an increasingly important part of their funding arsenal. “We will always prefer the loan product – it’s more flexible and has a shorter no-call period – but for optimal execution you need competitive tension in both markets,” he added. . said a source. “Also, since we are looking at larger transactions, it makes sense to use both loans and bonds. Europe isn’t the biggest market, and while there is a lot of cash available, you don’t want to find the bottom of it. “

To be sure, price pressure from the liquidity-rich bond market helped bring European loan market conditions back to almost the levels offered before the outbreak of the pandemic. According to LCD, single B-rated TLBs denominated in euros, for example, now expect a return of less than 4% on average for the first time in a year.

|

Likewise, in the secondary market, the sponsored part of the S&P European Leveraged Loan Index (ELLI) also returned to the levels last seen before the outbreak of the pandemic, as demand for the asset class in the first quarter of this year was strong and rising sharply. issuance of new money from redemptions has been offset by a number of massive repayments from borrowers such as Refinitiv US Holdings Inc., SCM Biogroup-LCD and INOVYN Ltd.

|

Dry powder

Despite the resumption of debt buyback issues in the first quarter, some market players remain disappointed. “Even though we are breaking records in terms of volume, there should have been more buyouts in this first quarter,” says a senior banker. “We have fallen behind schedule, given the amount of dry powder available in the market. Sponsors are holding assets longer, and soaring prices in public markets are pushing valuations higher, while infrastructure funds and families are buying. assets that would once have gone into private equity. There has been an expansion in business, sure, but we could have seen more of it. “

|

In the first quarter, the volume of dry powder available to private equity sponsors reached the highest level on record, according to data from Preqin. However, some sources note that private equity firms will soon be using those cash reserves in the service of revenge – especially after seeing how accessible the funding markets are today. “We’ve only really had this exuberance in the market since the New Year, and there’s a bit of a lag with the flow of M&A,” said one sponsor. “It’s a great market to sell in and the outlook looks very strong.”

Others note, however, that despite the availability of funding, sponsors face challenges in putting their dry powder to work, as valuations have been pushed up by soaring prices available in the stock markets. For some issuers in favored sectors such as tech, fintech and healthcare, sources say valuations rose five turns or more between last year and this year.

At the same time, some market participants argue that the strength of the stock markets is the biggest difference between the first quarters of 2020 and 2021. This factor not only impacted the comparable valuations required for buybacks, but also has meant that private equity firms see an increasingly attractive alternative to secondary auctions. “The stock markets are really exploding,” says a private equity banker. “The reality is that we are spending a lot more time than ever advising sponsors on stock exits.”

This is not to say, however, that the prices in the equity markets are insurmountable, and the sponsors note that there are still opportunities to find value in certain assets that have enabled private equity. For example, Nordic Capital’s offer for Advanz Pharma was recommended to shareholders in January, while Recipharm AB (publ) was delisted in early March after its acquisition by EQT.

|

ESG emerges

A final change observed in the buyout finance market between the first quarter of 2020 and the same period in 2021 was the introduction of environmental, social and governance-related pricing criteria on leveraged finance transactions. In Q1 2020, there were no ESG pricing mechanisms on buyback transactions, but this year the structures have become a familiar sight in European leverage finance markets.

In 2021, the leveraged loans backing the takeover of building materials distributor Stark Group A / S by CVC and backing the acquisition of mechanical and electrical drive manufacturer Flender GmbH by Carlyle both carried related margin ratchets. at ESG, the first agreement being linked to a reduction in greenhouse gas emissions and the latter linked to the power volume of new gearbox installations in wind turbines.

And the term loan portion of 845 million euros of the buyout financing of Asda has a margin ratchet of 5 basis points linked not to a specific objective linked to sustainable development, but to the ESG rating of the company. a third-party vendor company.

Although ESG-related prices were not included in any bond buyback transactions in the first quarter, there were two high-yield deals that included sustainability language – suggesting that such a structure could still be included in repurchase obligations in the future.

But the biggest impact of the market’s growing focus on ESG may come from the type of buyout seen in the market, as for some sponsors sustainability and ESG criteria have become a central part of their acquisition strategy. which will have an impact on the type of redemption. market sees in the future. “Over the past year, ESG has become a reality,” says a leading market player. “It has become an important aspect of the business models of some sponsors, where there is nothing in their portfolio that is not ESG focused. It is part of their philosophy. But there is also a certain bifurcation. there, and other sponsors are less concerned. “

Others note that this topic cannot be ignored for long by private equity sponsors. “ESG is a trend that’s here to stay,” says a private equity manager. “The LP [Limited Partners] demand it, and they expect us to be accountable. Even if it’s only from a fundraising standpoint, it makes sense to embrace it. “